Navigating the world of employee health benefits can be complex for both employers and employees. As healthcare costs continue to rise, businesses are seeking flexible, cost-effective solutions. One powerful tool gaining significant traction is the Health Reimbursement Arrangement (HRA). An HRA is an employer-funded health benefit plan that reimburses employees tax-free for qualified medical expenses, and in some cases, for individual health insurance premiums.

This comprehensive guide will unpack everything you need to know about Health Reimbursement Arrangements. We’ll explore the different types of HRAs, how they work, the significant benefits they offer to both companies and their staff, and the key rules that govern them. Whether you’re a small business owner looking for a better way to offer benefits or an employee trying to understand your options, this article will provide the clarity you need.

What Exactly is a Health Reimbursement Arrangement?

A Health Reimbursement Arrangement, or HRA, is an account-based health plan that an employer funds. It is not an account with a cash balance like a Health Savings Account (HSA). Instead, it is a promise by the employer to reimburse employees for eligible medical costs up to a certain dollar amount per year.

Here are the defining characteristics of an HRA:

- Employer-Funded: Only the employer can contribute to an HRA. Employees cannot contribute.

- Tax-Advantaged: Reimbursements received by employees for qualified medical expenses are tax-free. The employer’s contributions are also tax-deductible for the business.

- Notional Account: The funds are not typically held in a separate bank account for each employee. The employer only pays out the money when an employee submits a valid claim for reimbursement.

- Employer-Owned: The employer owns the HRA and sets the terms of the plan, including the allowance amount and what expenses are eligible. If an employee leaves the company, the HRA funds stay with the employer.

HRAs offer a level of flexibility and cost control that is difficult to achieve with traditional group health insurance plans, making them an attractive option for businesses of all sizes.

The Different Types of Health Reimbursement Arrangements

The HRA landscape has evolved significantly over the years. Today, there are several types of HRAs, each designed to meet different needs. Understanding these options is the first step in determining which might be the right fit.

1. Qualified Small Employer HRA (QSEHRA)

A QSEHRA is specifically designed for small businesses with fewer than 50 full-time equivalent employees that do not offer a group health insurance plan.

- How it Works: The employer sets a monthly allowance. Employees purchase their own individual health insurance plan (often from the Health Insurance Marketplace) and pay for medical expenses. They then submit proof of these expenses for tax-free reimbursement from the QSEHRA.

- Contribution Limits: The IRS sets annual contribution limits for QSEHRAs. These limits are adjusted each year for inflation.

- Key Feature: It empowers small businesses to help employees pay for insurance premiums and out-of-pocket costs without the administrative burden of managing a traditional group plan.

2. Individual Coverage HRA (ICHRA)

The ICHRA is one of the most flexible HRA options available and can be offered by employers of any size.

- How it Works: Similar to a QSEHRA, employers offer a monthly allowance for employees to purchase their own individual health insurance coverage. However, an ICHRA offers more flexibility. Employers can offer different allowance amounts to different classes of employees (e.g., salaried vs. hourly, full-time vs. part-time).

- No Contribution Limits: Unlike a QSEHRA, there are no government-imposed limits on how much an employer can contribute to an ICHRA.

- Key Feature: An ICHRA can be offered to some employees while a traditional group plan is offered to others, as long as the distinction is based on legitimate employee classes. This allows for greater customization of benefits strategies.

3. Group Coverage HRA (GCHRA)

Also known as an Integrated HRA, this type of plan works alongside a traditional group health insurance plan.

- How it Works: The employer offers a high-deductible group health plan (HDHP) to keep monthly premiums low. They then fund a GCHRA to help employees pay for their out-of-pocket costs, such as deductibles, copayments, and coinsurance.

- Example: An employee has a group plan with a $3,000 deductible. The employer offers a $1,500 GCHRA. The employee can use the HRA funds to cover the first $1,500 of their deductible expenses, significantly reducing their financial burden.

- Key Feature: It makes high-deductible plans more manageable for employees while keeping premium costs predictable for the employer.

4. Excepted Benefit HRA (EBHRA)

An EBHRA is a more limited type of HRA. It allows employers who offer a traditional group plan to provide an additional, modest HRA for employees to use on certain excepted benefits.

- How it Works: Employees can be reimbursed for things like dental and vision insurance premiums, short-term disability insurance, and copayments. It is not meant to cover medical insurance premiums.

- Contribution Limits: The IRS sets annual limits on EBHRA contributions.

- Key Feature: It’s a way for employers to offer extra perks and cover common expenses not typically included in a standard medical plan.

The Benefits of HRAs for Employers

Employers are increasingly turning to HRAs because of the significant advantages they offer over traditional health benefits models.

- Cost Control and Predictability: With an HRA, the employer’s maximum financial exposure is the total allowance amount they offer. There are no unpredictable premium increases from year to year. If employees don’t use their full allowance, the employer keeps the unused funds.

- Flexibility and Customization: HRAs, especially the ICHRA, allow employers to design a benefits plan that fits their specific budget and workforce. They can define employee classes and offer different allowance amounts accordingly.

- Reduced Administrative Burden: For small businesses, sponsoring a traditional group plan can be administratively complex. A QSEHRA or ICHRA offloads the task of choosing and managing a plan to the employee, simplifying the employer’s role to just providing the funding.

- Tax Advantages: Employer contributions are 100% tax-deductible as a business expense.

The Benefits of HRAs for Employees

The advantages extend to employees, who gain more control and choice over their healthcare.

- Plan Portability and Choice: With an ICHRA or QSEHRA, employees are not locked into a one-size-fits-all group plan. They can choose an individual plan from the Health Insurance Marketplace that has the network of doctors and level of coverage that best suits their family’s needs. This plan is portable, meaning they can keep it even if they change jobs.

- Tax-Free Funds: Reimbursements for premiums and qualified medical expenses are free from both income and payroll taxes. This is more valuable than an equivalent salary increase, which would be taxed.

- Coverage for a Wide Range of Expenses: HRA funds can be used for a vast list of IRS-approved medical expenses, including doctor visits, prescription drugs, dental care, vision care, and mental health services.

How Do Health Reimbursement Arrangements Work in Practice?

Let’s walk through a typical workflow for an employee using an ICHRA or QSEHRA.

- Employer Sets the Allowance: The company decides how much tax-free money to offer each employee per month. For example, an employer might offer a $400 monthly allowance.

- Employee Shops for a Plan: The employee goes to the individual health insurance market (e.g., HealthCare.gov or a state exchange) and purchases a plan that meets their needs. Let’s say they choose a plan with a $350 monthly premium.

- Employee Pays and Submits for Reimbursement: The employee pays the $350 premium to the insurance company. They then submit proof of payment (like an invoice or bank statement) to their employer or the HRA administrator.

- Employer Reimburses the Employee: The employer verifies the expense and reimburses the employee for $350, tax-free. This reimbursement is often added to the employee’s regular paycheck.

- Using Leftover Funds: In this example, the employee has $50 remaining in their monthly HRA allowance ($400 – $350). They can use this remaining amount to get reimbursed for other out-of-pocket medical costs, like a doctor’s copayment or a prescription.

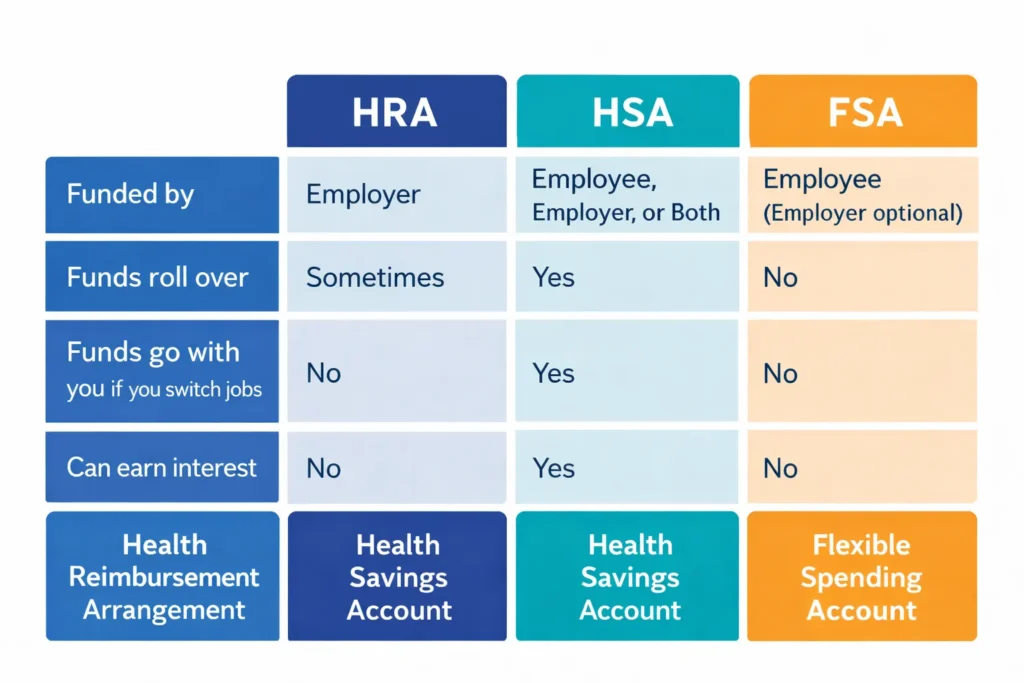

HRA vs. HSA and FSA: What’s the Difference?

HRAs are often confused with Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). While all are tax-advantaged health accounts, they have critical differences.

| Feature | Health Reimbursement Arrangement (HRA) | Health Savings Account (HSA) | Flexible Spending Account (FSA) |

| Who Funds It? | Employer only | Employer and/or Employee | Employer and/or Employee |

| Who Owns It? | Employer | Employee | Employer |

| Portability? | No. Stays with employer upon job change. | Yes. Employee owns and keeps the account. | No. Funds are forfeited upon job change. |

| Roll Over? | Employer’s choice. Can allow funds to roll over. | Yes. Funds roll over year after year. | Employer’s choice. Limited rollover or grace period may be offered. |

| Prerequisite? | Varies by HRA type (e.g., GCHRA requires a group plan). | Must be enrolled in a high-deductible health plan (HDHP). | Typically offered with a group health plan. |

Important Rules and Compliance Considerations

While HRAs are flexible, they are still formal benefit plans subject to federal regulations.

- Plan Documents: Employers must have formal plan documents that outline the terms of the HRA.

- ERISA and COBRA: Most HRAs are subject to ERISA (Employee Retirement Income Security Act) and COBRA continuation coverage requirements.

- Substantiation: Employers must have a process in place to verify that employees are using funds for legitimate, qualified medical expenses. This is why many businesses use third-party HRA administration software.

Conclusion: A Modern Solution for Health Benefits

Health Reimbursement Arrangements represent a significant shift in how employee benefits can be structured. They move away from a rigid, one-size-fits-all model toward one defined by flexibility, choice, and cost control. For employers, they offer a predictable and tax-efficient way to provide meaningful health benefits. For employees, they provide the freedom to choose a health plan that truly fits their needs, all while using tax-free dollars.

As the healthcare landscape continues to evolve, HRAs like the QSEHRA and ICHRA are becoming indispensable tools for businesses looking to attract and retain top talent without breaking their budget. They are a true win-win, empowering both employers and employees to take control of their healthcare journey.

FAQs About Health Reimbursement Arrangements

Can I contribute my own money to my HRA?

No. Health Reimbursement Arrangements can only be funded by the employer. If you want an account you can contribute to personally, you might consider an HSA or FSA if your employer offers one.

What happens to unused HRA funds at the end of the year?

This depends on the employer’s plan design. Some employers may allow a portion or all of the unused funds to roll over to the next year. In other plans, the funds are forfeited at the end of the plan year.

Are HRA reimbursements considered taxable income?

No. As long as the reimbursements are for qualified medical expenses as defined by the IRS, they are 100% tax-free for the employee.

Can I have an HRA and an HSA at the same time?

It can be complicated. Generally, you cannot contribute to an HSA if you are covered by a “general-purpose” HRA that reimburses all medical expenses. However, you may be able to have an HSA if your HRA is a “limited-purpose” HRA (e.g., only for dental and vision) or a “post-deductible” HRA.

What is a “qualified medical expense”?

The IRS defines a long list of qualified medical expenses in Publication 502. This includes costs for diagnosis, cure, mitigation, treatment, or prevention of disease. Examples include insurance premiums, doctor visit copays, prescriptions, dental treatments, and eyeglasses.

Sofia Bennett is a fashion writer and style observer known for her clean sense of aesthetics and trend analysis. She has covered fashion shows, reviewed designer collections, and interviewed independent creators. Sofia specializes in connecting fashion with real-life lifestyle choices, helping readers understand what looks good — and why.