If you’ve ever hired a contractor, cleaning service, or moving company, you’ve probably seen the phrase “licensed, insured, and bonded.”

But let’s be honest — most people nod along without really knowing what it means.

So what does bonded mean in a business, exactly? And more importantly, why should you care?

Whether you’re a homeowner hiring a service provider or a business owner trying to build credibility, understanding business bonding isn’t just a technical detail — it’s financial protection. In some cases, it’s the difference between recovering your money and losing thousands.

In this in-depth guide, I’ll walk you through:

- What “bonded” actually means (in plain English)

- How business bonds work behind the scenes

- The difference between bonded vs insured vs licensed

- Who needs to be bonded — and who doesn’t

- How to get bonded step-by-step

- Common myths and costly mistakes

- Practical examples from real-world scenarios

By the end, you won’t just understand the definition — you’ll know how to use it to protect your money or grow your business.

Let’s break it down.

What Does Bonded Mean in a Business? (Simple Definition)

At its core, when someone asks, what does bonded mean in a business, the answer is this:

A bonded business has purchased a surety bond that protects customers against financial loss if the business fails to fulfill its obligations.

Think of it like this:

- Insurance protects the business.

- A bond protects the customer.

That’s a huge distinction.

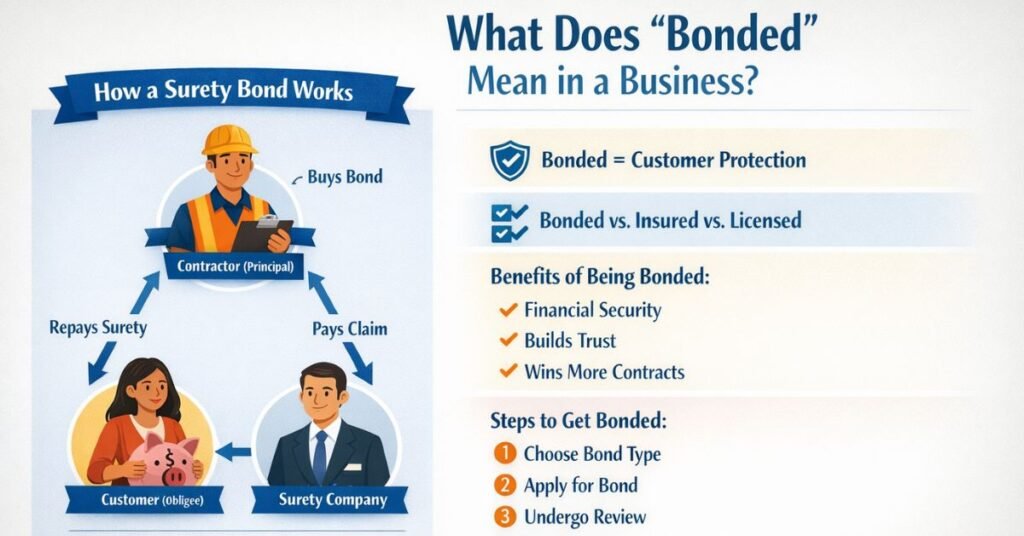

A surety bond is a three-party agreement:

- The Principal – the business buying the bond

- The Obligee – the customer or government entity requiring the bond

- The Surety – the company issuing the bond and guaranteeing payment

If the business fails to complete a job, violates regulations, or acts dishonestly, the customer can file a claim against the bond. If the claim is valid, the surety company pays the customer — and then the business must reimburse the surety.

That last part is critical. A bond is not insurance for the business. It’s a guarantee of performance or honesty.

In short:

Being bonded means there’s a financial safety net for your customers.

How Business Bonds Actually Work (Behind the Scenes)

To really understand what bonded means in a business, you need to understand how the money flows.

Let’s use a relatable example.

Imagine you hire a contractor to remodel your kitchen. They’re bonded for $25,000.

Halfway through the project, they disappear with your deposit.

Here’s what happens next:

- You file a claim against their surety bond.

- The surety investigates the claim.

- If valid, they compensate you up to the bond limit.

- The contractor must repay the surety company.

The bond doesn’t excuse bad behavior — it enforces accountability.

Here’s why this matters:

- It discourages fraud and negligence.

- It forces businesses to operate responsibly.

- It gives customers peace of mind.

Surety companies don’t issue bonds lightly. They review credit history, business experience, and financial stability. If a business has poor credit or a history of claims, getting bonded becomes expensive — or impossible.

So when you see “bonded,” it often signals financial credibility.

Bonded vs Insured vs Licensed: What’s the Difference?

This is where most confusion happens.

Let’s clear it up.

Licensed

A licensed business has met local or state requirements to legally operate. This might involve exams, training, or fees.

Insured

An insured business carries liability insurance. If someone gets injured or property is damaged, insurance covers those losses.

Bonded

A bonded business has purchased a surety bond that protects customers against contract violations or unethical behavior.

Here’s a quick comparison:

Licensed = Legal permission

Insured = Accident protection

Bonded = Customer financial protection

A business can be:

- Licensed but not bonded

- Insured but not licensed

- Bonded but not insured

Ideally, you want all three.

If you’re hiring someone for a high-value job — roofing, construction, electrical work — this trio matters.

If you’re running a service business, displaying all three builds immediate trust.

Types of Business Bonds (And When They’re Required)

When people ask what does bonded mean in a business, they often assume there’s just one type of bond. In reality, there are several.

Here are the most common types:

Contract Bonds

Used in construction projects. They guarantee that contractors will complete the project according to terms.

Includes:

- Bid bonds

- Performance bonds

- Payment bonds

License and Permit Bonds

Required by governments for certain professions. These ensure businesses follow regulations.

Common for:

- Contractors

- Auto dealers

- Mortgage brokers

- Plumbers

Fidelity Bonds

Protect clients from employee theft or fraud.

Common for:

- Cleaning companies

- Home health aides

- Financial services

Court Bonds

Required for legal proceedings (like appeals or guardianships).

Each bond serves a different purpose. The type you need depends on your industry and local regulations.

Why Being Bonded Matters for Customers

From a customer perspective, bonded status reduces risk.

Here’s what it gives you:

Financial Recourse

If the business fails to perform, you can file a claim.

Trust Indicator

Bonded businesses have undergone financial screening.

Professionalism

Reputable companies invest in credibility.

Imagine hiring a moving company to transport $20,000 worth of furniture. Would you feel safer knowing they’re bonded?

Of course.

Bonding doesn’t eliminate risk — but it adds accountability.

Why Being Bonded Matters for Business Owners

Now let’s flip the perspective.

If you run a business, being bonded:

Builds trust instantly

Helps win contracts

Is required for certain industries

Separates you from amateurs

In competitive markets, “licensed, insured, and bonded” is more than a tagline — it’s a conversion tool.

I’ve seen small service companies increase close rates simply by emphasizing bonding in their marketing.

Why?

Because customers equate bonding with professionalism.

Step-by-Step: How to Get Bonded for Your Business

If you’re a business owner wondering how to get bonded, here’s the process broken down clearly.

Step 1: Determine the Type of Bond You Need

Check local regulations or contract requirements.

Step 2: Gather Business Information

You’ll typically need:

- Business license

- Financial statements

- Credit history

- Business history

Step 3: Apply Through a Surety Company or Broker

Many specialize in small business bonds.

Step 4: Underwriting Review

The surety assesses risk. Credit score plays a major role.

Step 5: Pay the Premium

You don’t pay the full bond amount.

You pay a percentage (often 1–10% annually).

For example:

$50,000 bond × 2% premium = $1,000 per year

Step 6: Receive Bond Certificate

You can now legally operate or advertise as bonded.

Cost of Getting Bonded

The cost depends on:

- Bond type

- Required bond amount

- Credit score

- Business experience

- Industry risk

Strong credit? You might pay 1–3%.

Poor credit? It could be 10–15%.

That’s why improving your credit can dramatically lower bonding costs.

Common Mistakes People Make About Bonding

Misunderstanding What a Bond Covers

It doesn’t cover accidents — that’s insurance.

Thinking a Bond Replaces Insurance

They serve different purposes.

Not Checking Bond Validity

Customers should verify bond numbers.

Underestimating Claim Consequences

Claims can damage reputation and future bonding ability.

Choosing the Cheapest Bond Provider

Reputation and financial backing matter.

Real-World Examples of Bonded Businesses

Construction Contractors

Often required to carry performance bonds for public projects.

Cleaning Services

Frequently carry fidelity bonds to protect against employee theft.

Auto Dealers

Must carry license bonds in many states.

Freight Brokers

Often required to carry surety bonds to operate legally.

Bonding is especially common in industries handling money, property, or large contracts.

Who Typically Needs to Be Bonded?

Industries that often require bonding include:

- Construction

- Real estate

- Automotive sales

- Financial services

- Janitorial services

- Home improvement

- Government contractors

If your business involves handling client funds, entering contracts, or working in private homes — bonding is often required or strongly recommended.

Tools, Providers & Bonding Companies to Consider

When shopping for bonds, look for:

- A-rated surety companies

- Transparent pricing

- Strong customer support

- Online verification tools

Common places to obtain bonds:

- Specialized surety agencies

- Insurance brokers

- National bonding providers

Free vs Paid Help

Some agencies offer free bond quotes.

Paid consultants may help navigate complex contract bonds.

Always compare:

- Premium rate

- Claim support

- Renewal terms

- Cancellation policies

Conclusion: Why Understanding Bonding Gives You an Advantage

So, what does bonded mean in a business?

It means financial protection. It means accountability. It means credibility.

For customers, it’s a safety net.

For businesses, it’s a trust multiplier.

In today’s competitive marketplace, trust is currency. Bonding is one of the clearest signals of professionalism and responsibility.

If you’re hiring, verify bonding.

If you’re building a business, consider getting bonded.

It’s not just a checkbox — it’s a commitment.

FAQs

Does bonded mean insured?

No. Insurance protects the business. Bonding protects the customer.

Is bonding required for all businesses?

No. It depends on industry and local regulations.

How long does it take to get bonded?

Often 24–72 hours for simple bonds. Complex bonds may take longer.

Can you get bonded with bad credit?

Yes, but premiums are higher.

What happens if a claim is filed?

The surety investigates. If valid, they pay the customer — and you must repay the surety.

Michael Grant is a business writer with professional experience in small-business consulting and online entrepreneurship. Over the past decade, he has helped brands improve their digital strategy, customer engagement, and revenue planning. Michael simplifies business concepts and gives readers practical insights they can use immediately.